Getting a mortgage late on your credit report can be disheartening and there is too much contradicting information on the internet on what to do next to get this mortgage late removed from your credit report.

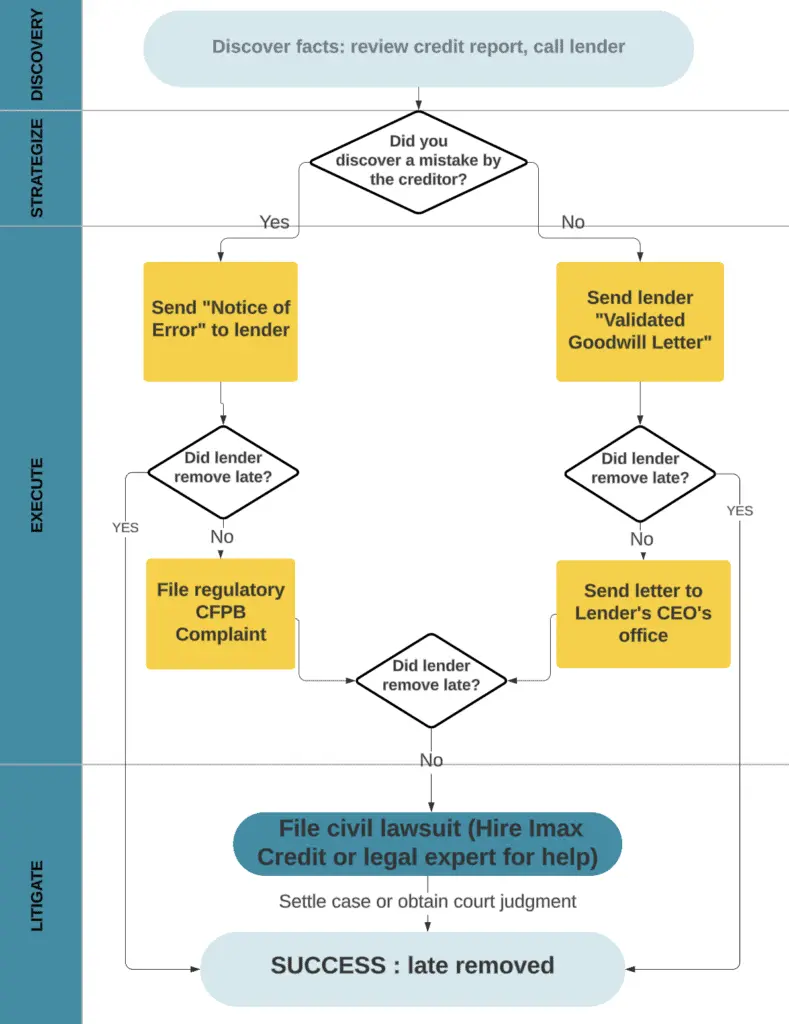

Over my 20 year career as a credit advocate, I’ve come up with my proprietary 4 step D.S.E.L Method on how to remove a mortgage late payment with any major mortgage company.

Step 1. Discover: find out of facts (why you were reported late)

Step 2. Strategize & Execute: Choosing what method to use: A “dispute backed by evidence” or a “validated goodwill request” backed by extenuating circumstances and Identification of errors that caused the late payment

Step 3: Escalate: Escalating your complaint with the creditor

Step 4: Litigate: Take legal action against the mortgage company yourself or HIRE US FOR THIS

Note that blindly sending template goodwill letters out will not work. Lenders do not remove lates based on goodwill

Read this Article on: How to remove a Freedom Mortgage late payment

Proof These Letters Work — Even on Old Inactive Accounts.

Results Gallery

The most dangerous thing about a mortgage late hitting your credit

If you’ve incurred a mortgage late within the last 12 months, you’re in danger of having your other credit cards % lines of credit shut down and your score dropping even more. What’s ridiculously unfair is card companies check your credit report every 3-12 months for ‘re-accessing your credit worthiness..”

If you had good credit prior to the mortgage late, then your score has dropped significantly. You’re now labelled a “high risk” and your other creditors may preempt by either closing out your credit cards or reducing credit limits .

If this happens you’ll have even less available credit and a reduced length of credit history. This will send your score into an endless downward spiral and dash your chances of getting any loans or cards.

Read this Article on: How to remove a Cenlar mortgage late payment

Study D.S.E.L method chart & watch my video on mortgage late payment forgiveness

I’ve flowcharted the D.S.E.L methodology below,. read it carefully. Leave your question in the comment section at the end if it’s unclear.

NEXT: Watch this video here

Read this article on : How to remove a Newrez Shellpoint Mortgage late payment,

STEP 1: DISCOVER FACTS- Review your credit report & call mortgage company

Before making a case for removal of the mortgage late payment, get your facts rights. Check your latest credit report history and then call the mortgage company to see what they have in their system and obtain the following information:

- 1) When and what payment amount was due ?

- 2) How many days was it late?

- 3) When and what payment amount was finally made to get the account current ? ( note: if you’re currently past due on your mortgage, immediately make your payment)

- 4) What month you were marked late for and what led to the late payment that they’re showing in their system?

- 5)Was the account late due to no payment being made, or was it a bounced check or an auto payment that didn’t go through?

- 6) Check your credit report to verify what month were you reported late.

- 7) Finally, combine these facts and write down the entire story in chronological order,

So #7 will help you compile the factual story to make your case. The entire “statement of fact” you write down may look something like this say if wanted to remove a United Wholesales Mortgage (UWM) late payment:

“For my United Wholesale Mortgage account (UWM) , June 1st payment due of $1341.54 was not made until July 10th $1381.42, when it had become 40 days late. Payment was late because I made an online payment on June 2nd for $1381.42 which bounced due to insufficient funds”

Now that you have facts from the lender, compare them with your own records & move on to the next stage.

Hire me to remove your mortgage late (You pay only after success )-

Over the last 20 years running Imax Credit Repair , I’ve helped thousands of clients remove late payments and have the Yelp Reviews to show.

My Guarantee. if late is not removed , you don’t pay!

📞 Call 323 983 8973

EMAIL ME: at mortgage@imaxcredit.com

Read this article on: How to remove a PHH Mortgage late payment

STEP 2: STRATEGIZE & EXECUTE- use “notice of error” or “validated goodwill letter”

If you couldn’t find any mistakes the mortgage company made, skip scanario 2.

Scenario 1: If you found a mortgage company error, send them a “Notice of Error letter”

If the mortgage missed payment occurred due to or in part of your mortgage company’s error, negligence or oversight, then you’re eligible to file a “Notice of error letter” dispute with the lender under RESPA. This may get the late removed. Here are some of the scenarios where you a notice of error letter will work, but you must have proof behind your claim :

- You were locked out of online access to your mortgage account, or the mortgage company’s system been consistently down.

- The company had the wrong spelling of your address or had your street # incorrect , due to which your mortgage statement were returned as “undeliverable” to the mortgage servicer.

- The mortgage company failed to update their system to your new mailing address or email address that you had provided to them before.

- The mortgage company’s phone rep took down your wrong bank account info when processing your payment.

- You set up an auto payment on the mortgage servicer’s websites which was canceled without you knowing OR you had previously set up a deferment with the mortgage company that they approved but still marked you late. (deferments can be granted for natural disasters).

- You paid the mortgage on time, but the mortgage lender failed to post the payment to your account.

- Your mortgage was taken over by a new servicer and you sent your payment to the old servicer

NOTE: Do NOT file a “notice of error” because the mortgage company failed to call you or failed to send you a notice that you were about to be marked late. Although its unfair, the FCRA does NOT require a mortgage lenders to call you or send you a written notice before marking you late on your credit report.

{Name}

{Mailing Address}

{Date}

Newrez / Shellpoint Mortgage

P.O. Box 10826

Greenville, SC 29603-0826

Mortgage ac# __________

Re: Error Resolution Notice under 12 C.F.R. §1024.35 (Regulation X)

I am submitting this Error Resolution Notice regarding the mortgage on my property at {Property Address}.

I was recently reported late for the payment due on {Month Day, Year}. I dispute this late payment because it was the result of an error for which your company is responsible.

This error occurred because _____________________ {insert detailed explanation of what happened, with dates, communication logs, or system errors. The more specific details provided, the stronger the dispute}.

At the time, I had sufficient funds in my account to cover the payment. For example, as of {Date}, my account balance was ${Amount}, well above the required monthly payment of ${Payment Amount}. Please see enclosed documentation as proof.

Therefore, under the Consumer Financial Protection Bureau’s Regulation X error resolution process (12 C.F.R. §1024.35), I request that you investigate this matter and correct my credit report by removing the late payment(s). Please notify me in writing of the results of your investigation within 30 days of receipt of this letter.

Best,

{Name}

Enclosed:

• Copy of bank statement showing sufficient funds

• {Other supporting documents proving the servicer’s error}

Scenario 2: If extenuating circumstances caused late, use “validated goodwill letter” below:

So goodwill letters and request do not work. However, if a third party’s mistake or a life circumstance (other than financial hardship) led to the late, then you can use what I call the “validated goodwill letter.” An example situation would be a natural disaster kept you from making a payment this would be Now lenders will remove lates based on a validated goodwill, however some lenders like Mr Cooper Nationstar Mortgage ,, Amerihome Mortgage, Arvest Mortgage do not honor “validated goodwill” removals, since they are not required to under the FCRA.

Here are some of the circumstances where a “validated goodwill letter” may work:

- You were hospitalized or suffering from emotional trauma.

- There was a death or emergency in the family.

- Your bookkeeper or accountant forgot to render payment.

- You had set up automatic payments through your own bank, and your bank made an error and did not process.

- Your email was hacked where you get e-statements, or the creditor’s emails ended up in spam.

- Your paper statements and mail was being stolen.

- You had submitted a double payment the month prior, mistakenly thought it would cover the next month.

- Your town was subjected to a natural disaster.

And below is a successful sample letter I’ve used in the past to get results

Validated goodwill letter to remove mortgage late payment(s)

{Name}

{Mailing Address}

{Date}

United Wholesale Mortgage

P.O. Box 619098

Dallas, TX 75261-9741

Mortgage ac# __________

Re: Mortgage Late Payment Correction

I am a satisfied customer of your company and am seeking help in resolving an issue which led to a late mortgage payment that was no fault of mine. I understand that you may consider extenuating circumstances and 3rd party errors in order to reverse late mortgage payments.

I was late for my mortgage payment by ___ days for the payment due on __.

This happened because _____________________ {insert one of the extenuating circumstances or 3rd party errors, and add VERY specific details — dates, correspondence, and documentation}.

In addition, I had sufficient funds in my bank account to make the payment had this circumstance not prevented it. At the time the payment was due for the month of ____, my account balance was $_____, which was well above the monthly payment due of $_____.

I understand under FCRA §1681 you are required to report accurate information. The intent of this law is to ensure reporting reflects true creditworthiness and risk of default. I am providing evidence to show this late was not due to financial inability or unwillingness to pay.

I have included my bank statement from that period as proof of my financial ability to pay, as well as proof of the circumstances that led to the late payment.

Best,

{Name}

Enclosed:

• Copy of bank statement

• Proof of extenuating circumstance or proof of 3rd party error

TIPS: The key to this letter working is proof of the third party’s mistake or proof of the extenuating circumstance. If possible, add a copy of your bank statement from the time of the missed payment to prove you had enough money at the time of the missed payment.

NOTE: If you didn’t have extenuating circumstances or errors: STOP and talk to a professional to see if there is a case based on other credit report coding violations

Read this article if you need a non-mortgage 30 day late payment removal

Listen to the podcast episode:

A single mortgage late payment can crush your score 📉 and cost you thousands of dollars 💵 in finance charges

If your’e financially responsible but let a late payment slip by for some reason, we can help you remove it and boost your credit score in the next 60 – 90 days

Let us help you fix it — starting with a free credit consultation.

Book Your Free ConsultationSTEP 3: ESCALATE- (use an option below based on your scenario)

Skip Option 1 and move to Option 2 if you sent a notice of error letter.

Scenario 1: if “validated goodwill letter” was denied, contact mortgage company’s CEO

I’ve removed late payment with Carrington mortgage and also Lakeview Loan Servicing by engaging their CEO’ on Linkedin , where I explained the situation and the circumstances surrounding my “validated goodwill request.”

Only use this step AFTER you’ve send in your validated goodwill request with proof .

What will not work is simply saying, ” hey , I’m a great customer I just forgot to make may payment.” That is an example of an “unvalidated goodwill.” This will NOT work.

Instead , you must refer to either a specific extenuating circumstance or a 3rd party error.

For example ” I was late due to a due to a death in the family and I’ve already submitted my family members death certificate on via certified

OR ” I was late since my licensed book keeping company failed to render payment and I’ve submitted a letter from my book keeping company to your mortgage company already via certified mail “

Note : do not email the CEO unless you have grounds for a “validated goodwill request” and have already mailed your “validated goodwill request” with proof and got denied by the mortgage company.

Here’s a sample letter to the CEO that I used on Linkedin which worked to remove a late payment :

Hello Mr [Last Name],

I am a current client with your mortgage company for my home located at [Property Address].

I had a 60-day mortgage late payment. This was due to my child being hospitalized during that time.

I previously sent correspondence to your company requesting removal of the late payment via certified return receipt mail. Enclosed in that request were proof of my child’s hospitalization and a copy of my bank statement showing a balance of ${Amount}. Despite this, the late payment still remains on my credit report.

I am respectfully requesting that your team review this request again and remove the late payment from my credit report, given the documented circumstances and supporting evidence.

Sincerely,

[Your Name]

Scenario 2: If “notice of error” letter was denied file CFPB complaint against the mortgage company

DO NOT not use Consumer Financial Protection Bureau (CFPB) for a “validated goodwill request.” Only utilize if there’s an error you can blame on the mortgage lender that played a part in the late payment. Why? Ironically, the CFPB discourages lenders from removing lates based on goodwill requests. If you’re make a “validated goodwill request”, you should instead write to the CEO or executive branch of the mortgage company ( see the next step for that)

The CFPB’s dispute resolution portal sends your complaint to the mortgage lender’s executive branch, and will send back any any responses they get from them . Here’s are the steps to file a CFPB complaint against the mortgage company:

How to file a CFPB complaint against the mortgage company?

📌 How to File a CFPB Complaint

- Go to the CFPB’s Complaint Portal.

- Enter your personal information. You’ll be prompted to provide your contact details.

- Verify your email. The CFPB will send you a confirmation link before you can proceed.

- Select the type of account. Choose “Mortgage”. If you are unsure of your loan type, select “Other” as well.

- Identify the problem. When asked “What type of problem do you have?”, select “Problem with credit report or credit score” and complete the follow-up questions.

- Submit your complaint details. Use the CFPB complaint template provided below. Once submitted, you will receive a response within 15–60 days. In most cases, mortgage companies respond in about 30 days.

Sample CFPB complaint for mortgage late removal due to lender error

CFPB Complaint Prompt: Describe what happened

On {Date}, I mailed my Notice of Error complaint to my mortgage lender under 12 C.F.R. §1024.35 (Regulation X). The mortgage company failed to correct my credit report that was impacted by this error. The mortgage company initially made an error on my account by _____________________ {describe in detail the fault of the mortgage company}.

I have attached a copy of my Notice of Error letter, along with proof of the error, in this complaint.

CFPB Complaint Prompt: What is the resolution you seek?

I am requesting that the mortgage company send an update to Experian, Equifax, TransUnion, and all other federal credit reporting agencies to correct my credit report and remove the late payments they reported. I am also requesting that they send me a credit update letter for my records, in the event the credit bureaus reinsert the lates on my credit report in the future.

Note: Filing a complaint does not guarantee a specific outcome, but it does put pressure on the mortgage company to address your concerns.

STEP 4: LITIGATE- Take legal action against mortgage company or HIRE ME to do it

The key is to find a professional who will only charge you AFTER success and not charge any upfront fees.

Over the last 20 years, I have helped hundreds of happy clients remove mortgage lates & have the YELP reviews to show for it

👉 Setup your FREE CONSULTATION

CALL (323) 983-8973

EMAIL ME at Mortgage@imaxcredit.com

FREQUENTLY ASKED QUESTIONS

How long does the mortgage late stay on the credit report

Any late payments will remain on your credit report for seven years from the time it was incurred. .

How long does it take for the credit score to improve after a mortgage late ?

Generally, you’ll recover half the lost points within a 24-36 month period. Grated that you maintain perfect overall credit from there onwards.

Example, if a 740 score drops to 640 due to a mortgage late, soon as the account becomes current again , they’ll gain maybe around 20 points. After that, the score would increase about 15-20 points yearly over the next 2 years. However, a single new late payment or deliquent account will eradicate those gains.

How many points does a mortgage late payment drop your score by ?

I feel the credit scoring system is very unfair to people with good credit scores, due to the additional financial repercussions they have to deal with. The score impact due to a missed mortgage payment varies according to someone’s prior credit history and score. A person with a good score will have a much more severe drop in score, as compared to a person with an already low score.

For example, Alex, a prior customer of mine, with perfect credit history had a great 740 credit score,. He missed a payment with Specialized loan Servicing. His Fico Scores (most commonly used version of credit scores by lenders) dropped over 80-100 points, thereby destroying his perfect credit.

What’s worse, within a 60 days, Alex’s credit card issuers closed down 3 of his credit cards and 2 other companies reduce his credit limits, This happens because card companies check your credit report every 3-12 months for ‘account review’ purposes.

His oldest tradelines were shut down. He ended up having less available credit and a reduced length of credit history. This kept dropped his credit score for months to come

On the contrary, if Alex had a below average credit history and score in the 500s, a new missed mortgage payment would have only dropped his credit score 10-20 points.

Will a mortgage company remove a late payment as a if I send a goodwill letter?

No… although it may have worked for some in the past for some, but in the current age, asking simply for a late payment forgiveness or writing a goodwill letter to the mortgage lender does NOT work. Want proof ? Bank websites like the one I’ve linked to here clearly state they’re “not able to honor request for goodwill adjustments” However, I have found that a “validated goodwill letter” or a “notice of error letter’ may work .

Here’s why goodwill don’t work : The CFPB has been pushing lenders to follow the Fair Credit Reporting Act, which requires all lates to be reported in an accurate manner. and requires them to remain in your report for seven years. So, lenders always tell consumers “according to the FCRA, our late mortgage payment policy doesn’t allow us to remove accurate late payments off your credit file.”

Over the last 20 years, I’ve seen hundreds of people send out generic goodwill letters and barely any have gotten their late payments removed. For approximately every 30 generic goodwill letters sent out, only one has worked, and that too probably because the mortgage company may have realized they made an error in not processing the consumers payment on time.

Likewise, to write a successful remove goodwill removal letter, it needs to be a “validated goodwill letter” where you need to prove either extenuating circumstances OR provable third party errors .

I discuss this in detail in the sections below section.

Should I do a credit bureau dispute to remove mortgage late payment(s)?

No, Gone are the days where a simple credit bureau dispute got lates off. Credit bureau disputes DO NOT work, despite some people online sharing rate success stories, here’s why…

I’ve done thousands of credit bureau disputes for clients. , For every 30 credit bureau disputes for mortgage lates only 1 or 2 would be successful and often be reversed the following month.

Yes, the FCRA gives you the right to dispute information, but what’s unfair is that when you dispute an account, the credit bureau investigation simply delegates the decision to the mortgage company.

For example following a credit bureau dispute , Experian will merely ask your mortgage company through system called e-oscar whether you were late or not. Contrary to popular belief, the lender is not required to provide any proof to Experian. They simply have to verify, either yes or no. And they do so with relative ease.

You’ll read a lot on the internet that if mortgage companies don’t respond to a credit bureau dispute within 30 days, the bureaus must delete. True, but mortgage companies, spend millions on their credit bureau reporting departments and they are always in FCRA compliance.

The only way a mortgage company won’t respond to a dispute, is if there is no record of you in their system, due to the mortgage company having purged your account records.

In conclusion, if the mortgage company is showing you as late in their system, then disputing with the credit bureaus won’t work.

What if you’ve been more than 60 days late or have numerous mortgage lates ?

If you have payments made over 60 day late appearing on your credit report, you may be able to remove them. You need a “validated claim” for removal or you have mistakenly reported late payments

This process will NOT work, if you have several scattered late payments over the years on your mortgage. If that is the case, the account may be removed with our professional help once the account is paid off.

When is a late mortgage payment reported to your credit report?

A mortgage payment is will only be reported late to the credit bureau if it is made 30 days after the due date, It may however incur a lat payment fee once its 15 days late

For instance, Cathy’s Newrez Shellpoint Mortgage statement shows a payment due on July 1st. Hence, she has 30 days or until from July 31st to pay before she late over 30 days. She won’t be marked late on her credit report if she makes her mortgage payment 1 day later on July 2nd or even 27 days after on July 28th .Some mortgage companies like Caliber Mortgage state you’re to make your payment within the calendar month.

Let’s assume Cathy makes her July mortgage payment on July 29th, then she will not be marked late by Shellpoint mortgage. However, Shellpoint may tack on a “late payment fee,” because mortgage lenders only allow a 15 calendar day “grace” period to avoid a mortgage late penalty fee.

So to simplify it:

July 1st: payment due date

July 15th: mortgage late payment penalty fee assessed (but not reported late to credit bureaus)

July 31st: reported late to credit bureaus (for missed June 1st payment )

Will a mortgage company remove a late payment from credit as a courtesy ?

With certain circumstances present present, the mortgage companies will instruct the credit bureaus to remove the late payments from your credit report. However, a courtesy or goodwill request is not enough.

So in order to remove a missed mortgage payment, you’ll need to make a good case, using a “validated goodwill request” that revolves around provable extenuating circumstances( life events). Another options is a “notice of error” argument based on mistakes made by the lender in servicing your loan. In this article, I’ll go over exactly how to make that case for either of those .

What will NOT work is generic goodwill requests to the mortgage company or online disputes with the 3 credit reporting agencies . More on that below.

Hire me to remove your mortgage lates (You pay only after success )-

Over the last 20 years running Imax Credit Repair , I’ve helped thousands of clients remove late payments and have the Yelp Reviews to show.

My Guarantee. if we don’t remove the late , you don’t pay!

📞 Call 323 983 8973

EMAIL ME: at mortgage@imaxcredit.com

I had a late with United Wholesale mortgage, I emailed UWM’s CEO, given that my mortgage was transferred from another letter to UWM and the auto pay disengaged What’s my next step and how can I hire you guys ?

Hi Patrick, I believe you’ve got a good case for deletion, per RESPA( Real Estate Settlement Procedures Act) the lender cannot report you late within 60 days of the transfer.

Now if the CEO’s office fails to respond, then please reach out to me personally at email: Mortgage@imaxCredit.com

So my auto pay got disconnected with Shellpoint/Newrez mortgage, I called the lender and have not gotten anywhere. Due to this late payment on my credit report , I’m unable to get a new mortgage for an investment property.

What are my options and do I have a case against Newrez?

Hi Arleta, sorry to hear about this. So when you reached out to Shellpoint/Newrez, what did they say about the auto pay and specifically what reason did they give you it was disconnected?

Now if they’re admitting that its a mistake they made this should be easy to solve, and a regulatory complaint or engaging their higher management would do the trick . however for eg. if they say the auto pay was disconnected due to the face that you setup an auto pay for 24 month and the 24 month period expired, then that would be a different issue. Feel free to email me with any questions at mortgage@imaxcredit.com

く my mortgage payments are reported as on time from jan-april, may30/30 june, then on time for July. Do I ask for the goodwill adjustment. I was marked late in may for being 34.00 short and I didn’t realize it. When i went back to make the payment the app was glitching and wouldn’t allow me access to make the payment.

Hi Vanika, who is the lender involved?

Mortgage lenders don’t do goodwill adjustments, they may however do a validated goodwill, where you can prove a life circumstance or if the mortgage company had made a small error, like not notified you that the payment has gone up.

happy to speak with you offline , email me directly at Mortgage@imaxCredit.com

Hi Vanika, sorry to hear about this.

As I stressed in the article, mortgage companies are prohibited from doing goodwill adjustments per the Fair Credit Reporting Act (FCRA)

If you’re going to make a request for removal ,it better be “validated goodwill” request, where you can prove some extraneous life circumstance that led to the late payment, or lender culpability , in terms of them not notifying you of the payment increase etc.

In any case, I’d be happy to go over options offline, email me at Mortgage@imaxCredit.com

Hi …I was part of a forbearance plan with Shellpoint Mortgage/ Newrez Mortgage and was verbally told this won’t affect my credit while under the plan…now they did report me to credit bureau for the 3 months I couldn’t pay but was under forbearance . They did a loan modification and somewhere in the small print I guess it said that it will get reported.

It wasn’t pointed out to me. I’m super upset.

Is there anything I can do ?

Thanks for the article. Very informative.

I had a mortgage transfer to United Wholesale Mortgage, from United Wholesale Mortgage (yes same name different company) effective June 1, 2025. Setup auto pay with new mortgage June 23rd which was approved July 1st via an email. Company did inform me via email that the autopay wouldn’t cover the July payment and payments would begin August 1st, 2025.

As a result, I happened to check website August 5th and saw the past due balance. I immediately paid the July and August balance but was told the past due was reported the day before. I had no idea account was past due and sounds like maybe they don’t have to tell you. Had they notified, would’ve paid immediately.

Through the mortgage company websites secure message system, did hear back from email support saying they don’t do “Courtesy Waivers” of past dues. I have not sent official letter yet requesting.

Any thoughts you may provide would be greatly appreciated. Never had any dings on credit after 46 years and trying to avoid. Thx!

Hi Jon, so the main thing here is to see if there were any mistakes that United Wholesale Mortgage (UWM) made.

In this case it seems they’re saying this is not their fault, although its unfair.

Legally they’re only required to send you a statment.

This would take professional help , we do get deletions from them frequently, as we take legal action against UWM often.

email me directly at mortgage@imaxcredit.com.

Hi, I’m active duty military and was affected with most recent military shut down. On top of that my tenants were 2 months behind on paying their rent so I had to cover 2 mortgages. I’ve never missed payment with Freedom Mortgage but I now have 30 days late: I paid on day 31, what are my options

Hi Lenae, so this can be categorized as a provable extraneous circumstance the led to the late first step is to call Freedom and ask them their policy in situations like this, and if they say you have a shot of removing the late, you’ll need to send them proof of your active military status.Now if they say they have no policy to remove lates for folks affected by the shut down , then email me at mortgage@imaxcredit.com